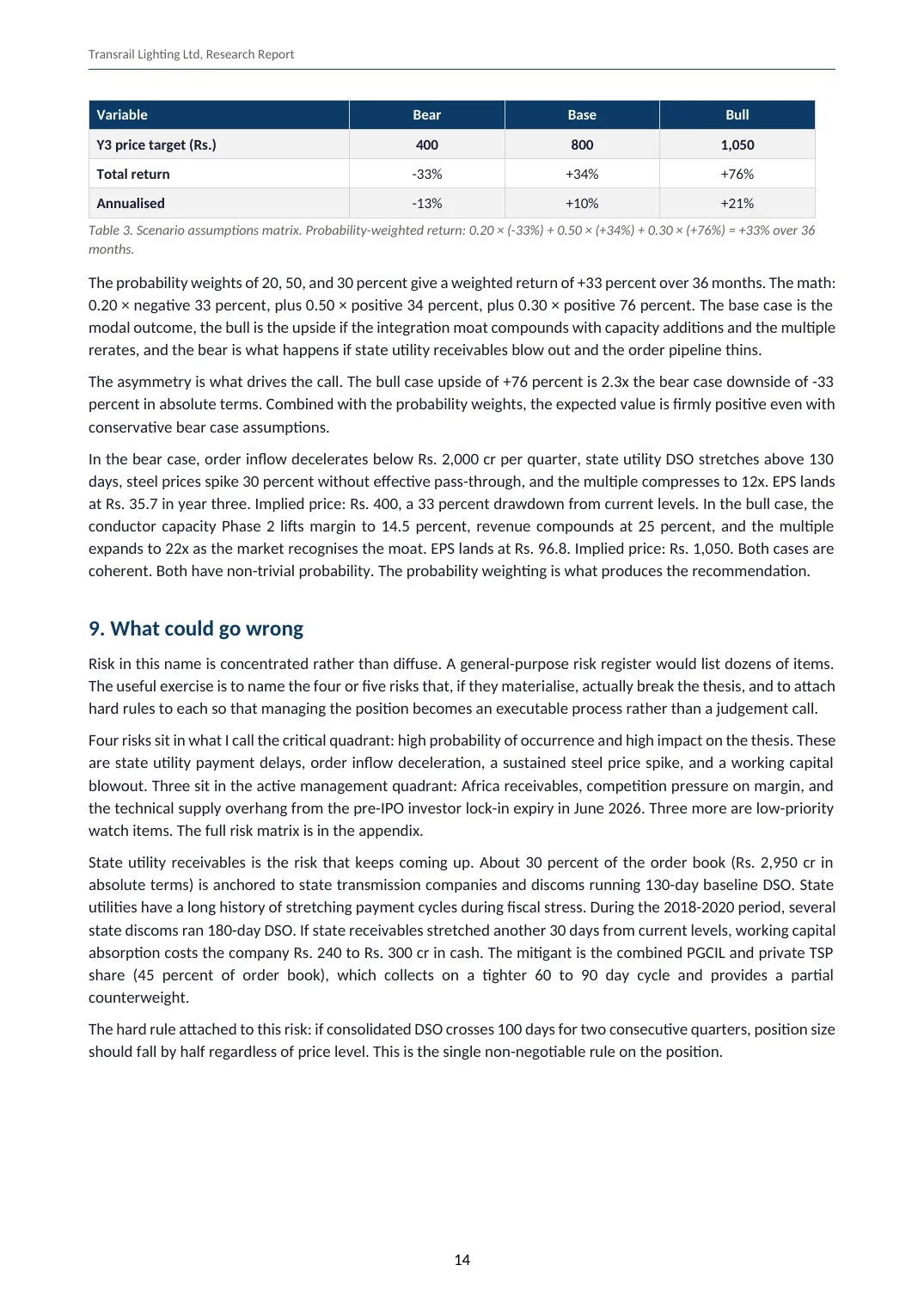

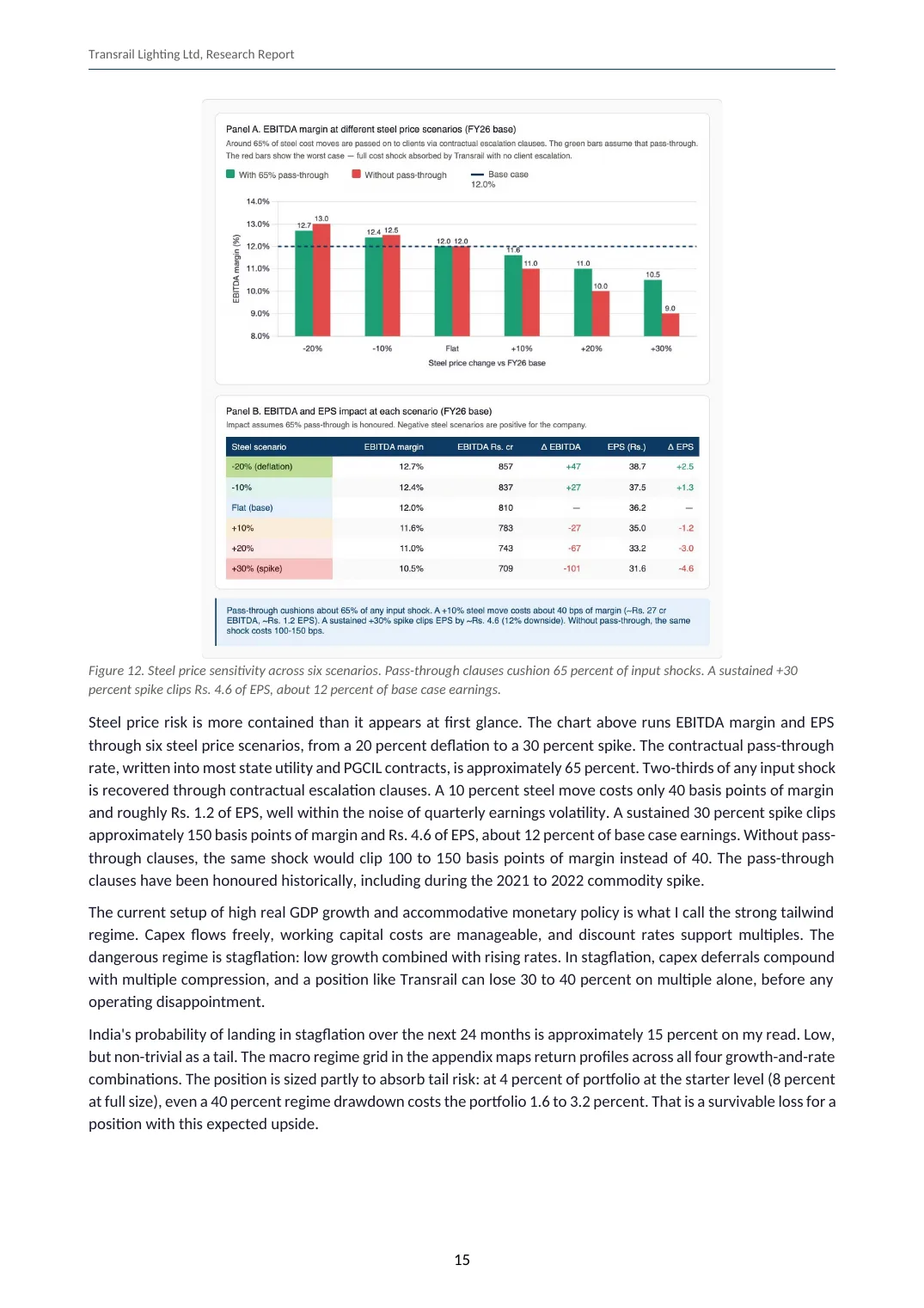

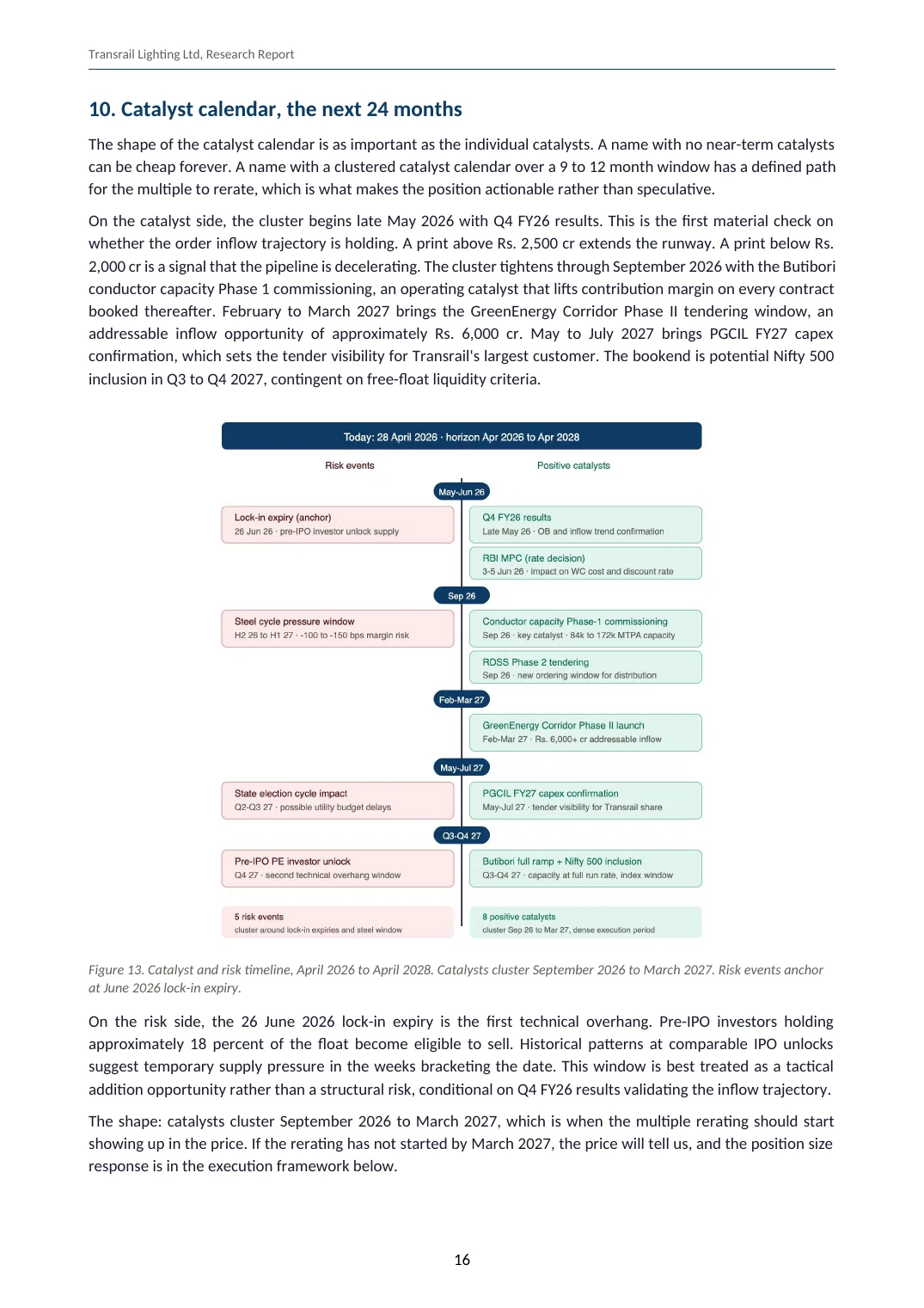

22 pages

22 pages29 Apr 2026

OpenSteel, Towers, and a Supercycle

Most power transmission contractors buy their steel towers. Transrail makes them in-house. On a 1000 crore contract, that gap is worth 40 crore of extra EBITDA. The stock trades at a discount to peers. Here is why that gap closes.

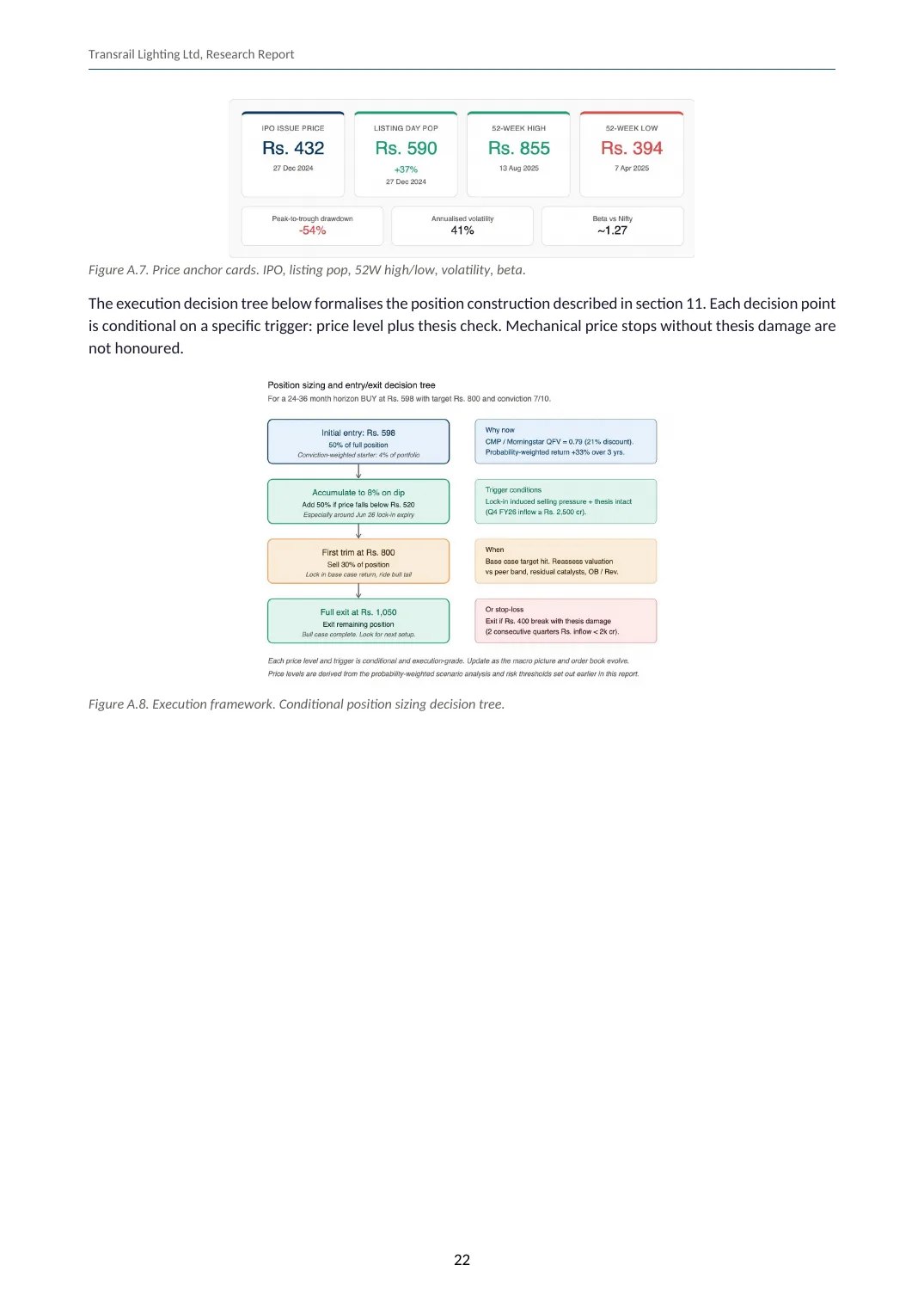

An equity research note on Transrail Lighting (NSE: TRANSRAILL), BUY at Rs. 598 with a 24-to-36 month target of Rs. 800. Probability-weighted return of +33 percent across bear, base, and bull cases. Three legs support the call: vertical integration into in-house tower fabrication captures 400 basis points of EBITDA margin per contract, India is entering its second power-transmission supercycle that takes the addressable annual market from Rs. 100,000 crore to Rs. 130,000 crore by FY28, and the stock trades at a discount to peers despite leading the group on growth, ROIC, EBITDA margin, and balance sheet leverage. Position sized at 4 percent of portfolio at starter level, 8 percent at full size.

▸ Where it stands

OpenLast reviewed 22 May 2026

- Entry

- 29 Apr 2026 · BUY at Rs 598

- Current view

- Thesis intact. FY27 transmission tender pipeline now visible at Rs 1.32 lakh crore, ahead of base case. Order book +18 percent QoQ in Q4 FY26. Position held at starter size.

Preview · 22 pages

Open full PDF → Page 1

Page 1 Page 2

Page 2 Page 3

Page 3 Page 4

Page 4 Page 5

Page 5 Page 6

Page 6 Page 7

Page 7 Page 8

Page 8 Page 9

Page 9 Page 10

Page 10 Page 11

Page 11 Page 12

Page 12 Page 13

Page 13 Page 14

Page 14 Page 15

Page 15 Page 16

Page 16 Page 17

Page 17 Page 18

Page 18 Page 19

Page 19 Page 20

Page 20 Page 21

Page 21 Page 22

Page 22

Have a sharper view on this? Send us a note →